Master Your Money with Zero-Based Budgeting

Learn how zero-based budgeting helps you control your finances, eliminate waste, and prioritize goals. A step-by-step guide for beginners.

If you're tired of watching your paycheck vanish without knowing where it went, you're not alone. Most people don't track their spending — they just hope there's something left at the end of the month.

That's where zero-based budgeting comes in. This simple yet powerful system helps you take full control of your money. Instead of wondering where your income disappeared, you'll assign every dollar a job — before you even spend it.

Let's break down how zero-based budgeting works, why it's effective, and how you can start using it today to transform your financial life.

What is Zero-Based Budgeting?

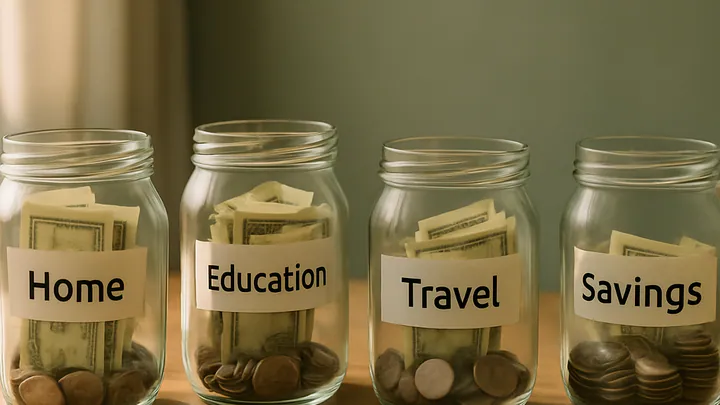

Zero-based budgeting (ZBB) doesn't mean having zero in your bank account — it means your income minus your expenses should equal zero. Every dollar you earn has a purpose. Whether it's for rent, savings, groceries, or fun, you plan exactly where your money will go.

Even your savings, debt payments, and entertainment get their own slice. When everything has a plan, nothing slips through the cracks.

Why Zero-Based Budgeting Works

This method works because it's rooted in intentionality. You're no longer guessing or leaving money unaccounted for. Here's why it's one of the best budgeting methods in 2025:

- It offers complete financial transparency

- Reduces impulsive spending

- Helps prioritize savings and debt payoff

- Works with any income and is highly adaptable

Zero-Based Budgeting: Step-by-Step Guide

1. Add Up Your Income

Include salary, side hustle earnings, freelance income — everything.

2. List All Your Expenses

Include both fixed and variable costs: rent, groceries, subscriptions, gym, fuel, etc.

3. Assign Every Dollar a Job

Match your total income to your expenses, savings, and debt — until it balances to zero.

4. Track & Adjust Weekly

Life changes, so your budget should too. Revisit and tweak it every week for accuracy.

Common Mistakes to Avoid

- Ignoring Irregular Expenses: Plan for birthdays, car repairs, and annual subscriptions with a "miscellaneous" or sinking fund.

- Overestimating Income: Budget using real, consistent income — not bonuses or overtime unless they're guaranteed.

- Being Too Rigid: Allow breathing room in your budget for spontaneity and enjoyment.

Start Small, Grow Big

You don't need to be a finance expert to see results with zero-based budgeting. Whether you're saving for a vacation, paying off debt, or just trying to stop living paycheck-to-paycheck — this system brings clarity and control. You can use a budgeting app, spreadsheet, or even pen and paper. The method remains effective as long as you stay consistent.

Real-Life Impact

When I started using zero-based budgeting, it changed everything. I felt empowered, clear-headed, and confident in every financial decision. My spending was guilt-free, and my savings grew faster than I thought possible.

This method isn't about restriction — it's about freedom.

Free Zero-Based Budget Template

Ready to take the leap? Grab your free zero-based budgeting template — a clean, printable tool to help you get started right now. Just drop your email, and it'll land straight in your inbox.

FAQs

Q: Is zero-based budgeting good for beginners?

Absolutely. It's simple, transparent, and helps even first-timers gain control over their finances.

Q: Can I use ZBB with a variable income?

Yes! Just budget based on your lowest expected monthly income to stay safe and adjust from there.

Q: Do I have to track every dollar?

Yes — that's the point! But you can make it easier using apps or premade templates.

How Zero-Based Budgeting Compares to Other Popular Methods

It helps to understand where ZBB sits alongside other budgeting approaches you might have already heard of.

- The 50/30/20 rule splits your income into needs, wants, and savings using fixed percentages. It's easy to start but leaves a lot of dollars untracked within each category — meaning sneaky overspending still happens.

- Envelope budgeting is ZBB's cash-based cousin. You physically stuff envelopes with cash for each category. It works well for people who overspend on cards, but it's impractical for online bills and digital payments.

- Pay-yourself-first budgeting moves savings out immediately, then spends the rest freely. It's great for building savings but doesn't address where the remaining money actually goes.

Zero-based budgeting is the most thorough of the three. It takes more upfront effort, but that effort is exactly what makes it so effective — especially if you've tried the other methods and still feel financially scattered.

Tools That Make Zero-Based Budgeting Easier

You don't have to do this with a pencil and a yellow legal pad (though you absolutely can). Here are some practical options depending on how hands-on you want to be:

- YNAB (You Need a Budget): Built specifically around the zero-based philosophy. Every dollar gets assigned as soon as it hits your account. It syncs with bank accounts and has a solid mobile app. There's a learning curve, but most users say it clicks within two to three budget cycles.

- Google Sheets or Excel: Free and completely customizable. Search for a ZBB template, plug in your numbers, and you're set. This works especially well if you like seeing everything laid out visually and want full control over categories.

- EveryDollar: A beginner-friendly app designed around zero-based budgeting. The free version requires manual entry, which some people actually prefer — it keeps you more aware of each transaction.

- Pen and paper: Still a legitimate option. Writing down your budget by hand forces you to slow down and think carefully about each category, which can actually lead to better decisions than tapping through an app.

The tool matters far less than the habit. Pick whichever format you'll actually open every week.

What to Do When Your Budget Doesn't Balance the First Time

Most people sit down for their first ZBB session, add up their income, list their expenses — and immediately realize the numbers don't match. That's completely normal, and it's actually the point. Here's how to work through it:

- Look at subscriptions first. Most households carry four to six subscriptions they've forgotten about — streaming services, app trials, annual renewals. These are easy to cut or pause without any real lifestyle change.

- Separate wants from needs within each category. Your "groceries" line might actually include snacks, specialty items, or convenience foods that belong in a "dining/entertainment" category. Splitting them reveals where you actually have flexibility.

- Temporarily reduce savings contributions. If the budget is deeply in the red, it's better to save a smaller amount consistently than to set an unrealistic goal and abandon the whole system by week two.

- Add an "overflow" category. Instead of letting leftover dollars sit undefined, give them a label — "next month's buffer," "emergency top-up," or "fun fund." Named money gets spent intentionally.

A budget that doesn't balance on day one isn't a failure — it's information. It's showing you exactly where the friction is, which is the most valuable thing a budget can do.