High-Yield Savings in 2026: Get More From Cash

A practical 2026 guide to high-yield savings accounts: how they work, what to compare, common pitfalls, and how to build a smarter cash strategy that outpaces regular banks.

TL;DR: A high-yield savings account (HYSA) is the simplest upgrade most people can make to their cash strategy in 2026. It works like a normal savings account, but pays a much higher annual percentage yield, is federally insured when you stay within limits, and takes about ten minutes to open. In this guide, we walk through how HYSAs work, what to compare, where they fit alongside checking and investing, and the small mistakes that quietly cost savers money.

Why high-yield savings matter more than ever in 2026

For years, the default advice was to keep an emergency fund at your local bank and accept whatever rate it offered. That advice made sense when rates everywhere were near zero. It makes far less sense now. Online banks routinely offer yields many times higher than the national average paid by traditional brick-and-mortar branches, and the gap has become one of the largest quiet drains on household finances.

Our team has watched readers move an idle emergency fund from a legacy bank into an online HYSA and immediately start earning meaningful interest each month without changing their spending, taking on risk, or locking up their money. It is one of the highest-leverage financial moves available, and it costs nothing.

How high-yield savings accounts actually work

An HYSA is a deposit account at a bank or credit union that pays a variable annual percentage yield (APY). The bank lends out or invests deposits and shares part of the return with you. Because online-first banks do not maintain expensive branch networks, they can pass more of that return to depositors, which is why the highest APYs almost always come from digital banks or credit unions rather than the largest national chains.

A few mechanics worth understanding:

- Interest compounds regularly. Most HYSAs compound daily and pay out monthly, so your interest starts earning interest quickly.

- The rate is variable. When broader short-term rates move, HYSA APYs generally follow. Your rate today is not a promise about next year.

- Access is easy, but not always instant. Transfers to an external checking account usually take one to three business days, though many banks now offer same-day options.

- Deposit insurance protects your principal. At FDIC-insured banks and NCUA-insured credit unions, your money is protected up to the standard limits per depositor and ownership category.

What to compare when choosing an account

Chasing the single highest advertised APY is a common mistake. A slightly lower rate at a well-designed bank is usually a better long-term choice than a flashy promotional rate that resets in three months. Here is the checklist we recommend using.

1. The realistic APY, not the promo rate

Check what the account pays after any introductory bonus expires. If the ongoing rate is uncompetitive, the bonus does not matter. Also look for tiered structures where the top rate requires a very large balance or specific behaviors.

2. Fees and minimums

The strongest online HYSAs typically have no monthly maintenance fee, no minimum balance requirement, and no fee to open the account. If an account charges any of these, keep looking.

3. Deposit insurance

Confirm the institution is FDIC-insured (banks) or NCUA-insured (credit unions). If you use a fintech app that partners with a network of banks, make sure the disclosure clearly explains where your money is held and how coverage works.

4. Transfer speed and limits

Test how quickly the bank moves money to and from your primary checking account. Some banks still cap the number of certain outbound transactions per month, though this has loosened in recent years.

5. App and customer service quality

A great APY is undermined by an app that crashes at the worst moment. Read recent reviews with a skeptical eye, and confirm there is a real customer support channel — phone, chat, or secure message — with human coverage.

6. Sub-account or bucket features

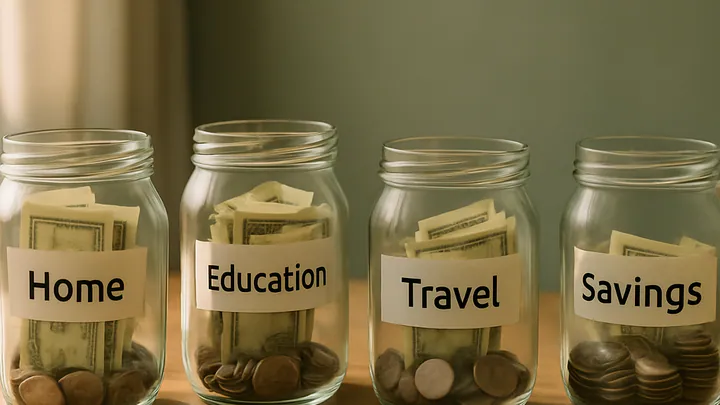

Some HYSAs let you split one account into labeled buckets for different goals, which is enormously useful for sinking funds like travel, car maintenance, or holidays.

Where an HYSA fits in your overall money map

An HYSA is not meant to replace every other account. It is the middle layer of a simple three-part cash structure that works well for most households.

- Checking account: Holds one to two months of core expenses. Used for daily bills and debit card spending.

- High-yield savings: Holds your emergency fund and short-term goals — anything you might need within roughly five years.

- Investment accounts: Retirement and long-term brokerage accounts for money you will not touch for many years.

The HYSA is the buffer between daily life and long-term investing. It keeps you from selling investments in a downturn to cover a car repair, and it keeps a large pile of cash from sitting idle in a low-rate checking account.

A simple setup you can copy this weekend

If you are starting from scratch, here is a straightforward workflow.

- Open one HYSA at a reputable online bank or credit union.

- Link it to your existing checking account.

- Move your emergency fund into it — most guidance suggests aiming for three to six months of essential expenses, adjusted for your job stability and dependents.

- Set up an automatic weekly or biweekly transfer, even if it is small. Automation matters more than amount.

- If your bank supports sub-accounts, create buckets for your specific goals: emergency, travel, home repairs, gifts, and so on.

Revisit the account every six to twelve months. If the APY has drifted well below competitors and stayed there, it may be worth moving. But do not chase every ten-basis-point difference — the friction usually is not worth it.

Common mistakes we see savers make

- Keeping a huge balance in checking. Anything above one to two months of expenses is usually wasted earning power.

- Confusing HYSAs with investing. They are a place to hold cash, not a growth engine. Long-term wealth still comes from diversified investing.

- Ignoring insurance limits. If your balance approaches the standard deposit insurance limit at one bank, consider spreading funds across institutions or ownership categories.

- Opening too many accounts. Managing five HYSAs across five banks becomes its own tax and paperwork burden. One or two is usually plenty.

- Forgetting about taxes. Interest is taxable income. Set aside a portion if you have a large balance, and expect a tax form from your bank each year.

HYSAs vs. money market accounts vs. CDs

These three cousins get compared often. In broad strokes: a money market account is very similar to an HYSA, sometimes with check-writing privileges and slightly different rate structures. A certificate of deposit (CD) locks your money up for a fixed term in exchange for a rate that will not drop during that period. CDs make sense for money you truly will not need until a known date. For a flexible emergency fund, an HYSA is almost always the better fit because you can withdraw without penalty.

Key takeaways

- A high-yield savings account is the easiest upgrade for idle cash — same access, much better yield.

- Prioritize the ongoing APY, low fees, deposit insurance, and a solid app over any promotional headline rate.

- Use your HYSA as the middle layer between checking and investing, sized to hold your emergency fund and short-term goals.

- Automate contributions and revisit your account once or twice a year — do not obsess over every rate change.

- Remember that interest is variable and taxable; plan accordingly.

Editorial disclosure: This article is for general educational purposes and does not constitute financial, tax, or investment advice. Rates, fees, and insurance rules change, and individual circumstances vary. Please consult a qualified financial advisor or tax professional before making decisions about your savings and cash management strategy.

Frequently asked questions

What is a high-yield savings account?

A high-yield savings account (HYSA) is a deposit account, usually offered by online banks or credit unions, that pays a significantly higher annual percentage yield than a traditional savings account while still offering easy access to your money.

Are high-yield savings accounts safe?

Accounts at FDIC-insured banks or NCUA-insured credit unions are protected up to the standard insurance limit per depositor, per institution, per ownership category. As long as you stay within those limits, your principal is protected even if the bank fails.

How often does the interest rate change?

HYSA rates are variable and can change at any time. They typically move in the same direction as broader short-term interest rates, so your APY can rise or fall over the course of a year without notice.

Should I keep my emergency fund in a high-yield savings account?

For most people, yes. An HYSA offers same-day or next-day access to cash while still earning meaningful interest, which is a better fit for emergency savings than certificates of deposit or investment accounts.

Can I have more than one high-yield savings account?

Absolutely. Many people use multiple accounts to separate goals like an emergency fund, travel savings, and a home down payment. Just be mindful of any monthly transfer limits and minimum balance rules at each bank.

Do I owe taxes on savings account interest?

Yes. Interest earned in a standard savings account is generally treated as taxable income in the year it is credited. Your bank will typically issue a tax form summarizing the interest you earned.