Sinking Funds in 2026: Plan for Every Big Expense

Sinking funds turn unpredictable bills into calm, planned saving. Here's how to set them up in 2026 so no expense ever blindsides your budget again.

TL;DR: Sinking funds are small monthly savings buckets earmarked for specific upcoming expenses — car repairs, holidays, insurance premiums, annual subscriptions, vet bills. Instead of treating these as surprises, you plan for them. In 2026, with high-yield savings accounts still paying meaningful interest and most banks offering named savings buckets, sinking funds are one of the simplest, most effective ways to stop the monthly cycle of budget chaos.

If you've ever wondered why your budget looks perfect on paper but falls apart every couple of months, the answer is usually the same: irregular expenses. Birthdays, car tires, the dentist, holiday travel, the once-a-year software renewal. None of them are emergencies. All of them are predictable. And almost none of them live in a typical monthly budget.

That's the gap sinking funds are designed to close. We've found them to be the single most underrated budgeting tool — quiet, unglamorous, and remarkably effective.

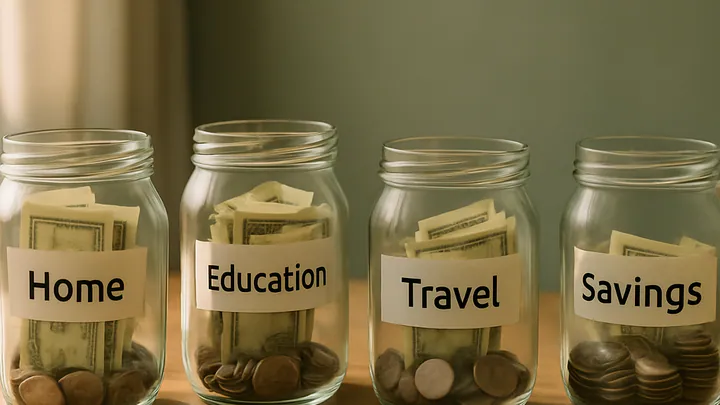

What a sinking fund actually is

A sinking fund is money you deliberately set aside, a little at a time, for a known future expense. The term comes from old corporate finance, where companies would set aside funds to retire debt — but the household version is simpler.

You decide what the expense will cost, when it's due, and divide the total by the number of months you have. That monthly number becomes a line in your budget, just like rent or groceries. When the expense arrives, the money is already there.

The magic is psychological as much as mathematical. A $1,200 annual car insurance premium feels like a crisis. The same amount saved as $100 per month feels like nothing.

Sinking fund vs. emergency fund

These two tools get confused often, but they do different jobs:

- Emergency fund: covers genuinely unexpected events — job loss, urgent medical care, a broken furnace in February. You don't know when, and you don't know how much.

- Sinking fund: covers expenses you do know about — the holidays happen every December, your registration renews every year, your dog needs annual shots.

Using your emergency fund for predictable expenses is one of the most common budgeting mistakes we see. It drains the cushion that's supposed to protect you from the truly unexpected.

Why sinking funds matter more in 2026

A few things have changed in the last couple of years that make sinking funds especially worthwhile right now.

Annual subscriptions have multiplied. Streaming services, cloud storage, password managers, AI tools, software licenses — many of them now offer steep discounts for paying yearly. Those once-a-year charges add up to real money, and they're easy to forget about until the credit card statement arrives.

Big-ticket categories have gotten more expensive. Car repairs, home maintenance, travel, and insurance premiums have all risen meaningfully in recent years. The cost of being caught off guard is higher than it used to be.

High-yield savings is still rewarding. Online banks continue to offer competitive rates on cash savings. Money sitting in a sinking fund for ten months isn't dead money — it's earning, modestly but meaningfully, while it waits.

The categories worth funding

You don't need a sinking fund for every line item in your life. Start by looking back at the past 12 months and asking: which expenses caught me off guard or forced me onto a credit card?

The most common, useful categories we see include:

- Car costs: repairs, tires, registration, annual inspection

- Home maintenance: HVAC service, gutter cleaning, appliance repair, small renovations

- Insurance premiums: if you pay annually or semi-annually for a discount

- Holidays and gifts: December alone, plus birthdays and weddings

- Travel: the trip you take every year, even if you don't always book it in January

- Annual subscriptions: a single bucket for all the yearly renewals

- Medical and dental: deductibles, glasses, dental work, planned procedures

- Pets: annual checkups, vaccinations, grooming, the occasional emergency vet visit

- Clothing: seasonal refreshes, work wardrobes, kids growing out of everything

- Tech replacement: phones, laptops, headphones — they all eventually die

Three to eight categories is a sensible starting range. More than that gets hard to maintain. Less than that and you'll keep getting blindsided.

How to set up your sinking funds

Here's the process we recommend walking through, ideally with a coffee and an hour of quiet.

1. List your real annual expenses

Pull up the last 12 months of bank and credit card statements. Highlight every charge that wasn't a normal monthly bill. You're hunting for the ones that made you wince.

2. Estimate next year's totals

For each category, write down a realistic annual number. Round up rather than down. If car repairs cost you $850 last year, budget $1,000 for this year. Things rarely get cheaper.

3. Divide by the months you have

If an expense is due in December and it's January, divide by 12. If it's due in June, divide by 6. The result is your monthly contribution. Add those contributions together — that's the total you need to redirect from your monthly budget into sinking funds.

4. Open the right account

A high-yield savings account at an online bank works well for most people. Look for one that lets you create named sub-accounts or savings buckets so each fund stays visually separate. Some banks call these "goals" or "spaces." If yours doesn't, a simple spreadsheet tracking balances inside one account works fine.

5. Automate the transfer

Set up an automatic transfer for the day after payday. This is the step that turns intention into reality. Money you don't see, you don't spend.

6. Review every quarter

Life changes. New car, new pet, dropped subscription, kid starting an activity. A 15-minute quarterly review keeps your funds aligned with reality.

Common mistakes to avoid

Sinking funds are simple, but a few pitfalls trip people up:

- Too many categories. If you can't remember what each fund is for, you have too many. Consolidate.

- Underestimating amounts. Looking at last year's spending is a starting point, not a ceiling. Build in some cushion.

- Raiding funds for unrelated spending. The car fund is for the car. If you keep borrowing from it for groceries, your monthly budget is the real problem.

- Treating them like investments. This is short-term cash. Keep it in savings, not stocks. The point is reliability, not return.

- Forgetting to start small. You don't have to launch ten funds on day one. Pick the two or three expenses that have hurt the most and start there.

A small worked example

Imagine you know your annual car insurance is $1,200, holiday spending is roughly $900, and you set aside $600 a year for car maintenance. That's $2,700 a year, or $225 a month moved into sinking funds.

It feels like a lot until you compare it to the alternative: three separate financial gut-punches across the year, each one potentially landing on a credit card at high interest. The monthly contribution is almost always cheaper than the cost of being unprepared.

Key takeaways

- Sinking funds turn predictable-but-irregular expenses into calm, planned monthly saving.

- They are not the same as an emergency fund — keep the two separate.

- Start with three to eight categories based on what has actually disrupted your budget in the past year.

- Use a high-yield savings account with named buckets, and automate the transfer the day after payday.

- Review quarterly and round your estimates up, not down.

- The goal isn't perfection — it's removing the surprise from your money life.

Editorial disclosure: This article is for general informational purposes only and does not constitute financial advice. Your situation is unique, and the right savings strategy depends on your income, debts, goals, and risk tolerance. For decisions about your specific finances, please consult a qualified financial advisor or accountant.

Frequently asked questions

What is a sinking fund?

A sinking fund is money you set aside gradually for a specific, expected expense — like a car repair, holiday gifts, or annual insurance. Instead of being surprised by a big bill, you save a little each month so the cash is already waiting when the expense arrives.

How is a sinking fund different from an emergency fund?

An emergency fund covers unexpected events like job loss or a medical emergency. A sinking fund covers expenses you know are coming but that don't happen every month, such as property taxes, vet visits, or a wedding you've been invited to.

How many sinking funds should I have?

Most people do well with three to eight categories. Too few and you'll miss real expenses; too many becomes hard to track. Start with the categories that have ambushed your budget in the past year and grow from there.

Where should I keep my sinking funds?

A high-yield savings account works well because the money stays accessible while earning interest. Many banks let you create named sub-accounts or savings buckets so each fund stays visually separate without opening multiple accounts.

Can I use one savings account for all my sinking funds?

Yes, as long as you track each balance in a spreadsheet or budgeting app. The money can sit in one account, but you should always know how much belongs to each category so you don't accidentally overspend.

What happens if I underfund a category?

If the bill arrives before the fund is full, you can pull the shortfall from your buffer, slow contributions to lower-priority funds that month, or use part of your emergency fund as a last resort and refill it quickly.

Are sinking funds worth it if money is tight?

Often, yes — even small amounts help. Saving a modest amount monthly for car repairs or annual fees is usually less stressful than facing the full bill at once or charging it to a credit card.