Sinking Funds in 2026: Budget for What's Coming

Sinking funds turn surprise expenses into planned ones. Here's how we set them up in 2026 to smooth cash flow, dodge debt, and stop raiding our emergency savings.

TL;DR: A sinking fund is a small, dedicated pool of cash you build up over time to cover a specific upcoming expense — annual insurance, holidays, car repairs, a vacation. In 2026, with everyday costs still climbing and credit card rates painful, sinking funds are one of the simplest ways to stop reacting to bills and start planning for them. Below, we walk through how to choose categories, set realistic monthly contributions, where to park the money, and how to keep the system running without burning out.

Most budgets break in the same place: not on coffee or takeout, but on the lumpy, irregular expenses that show up two or three times a year. The car needs new tires. Insurance renews. The holidays arrive on schedule, somehow always as a surprise. Sinking funds fix that pattern by turning irregular costs into predictable monthly line items.

What a sinking fund actually is

The term comes from old corporate finance, where companies set aside money gradually to pay off a future debt. The personal-finance version is friendlier: you pick an expense, divide its cost by the number of months until it's due, and save that amount each month. When the bill arrives, the money is already there.

That's the whole mechanic. The power isn't in the math — it's in the reframing. A $1,200 annual insurance premium stops being a once-a-year shock and becomes a calm $100 monthly habit.

Sinking fund vs. emergency fund

These two get confused constantly, and mixing them up is how people end up with a drained emergency fund every December.

- Emergency fund: covers the unknown. Job loss, urgent medical bills, a surprise home repair. It should sit untouched until something genuinely unexpected happens.

- Sinking fund: covers the known. Things you can see coming on a calendar or know will happen eventually, even if you don't know the exact date.

Holidays are not an emergency. Car maintenance is not an emergency. Treating them like one slowly erodes the cushion that's supposed to protect you from real surprises.

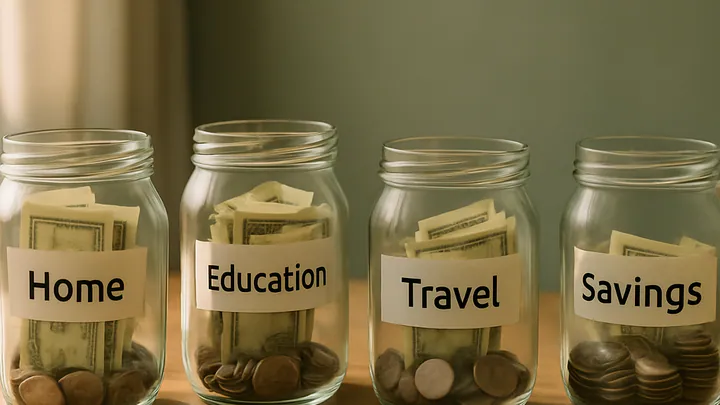

The categories worth setting up first

We've seen people build elaborate spreadsheets with twenty sinking funds and abandon the whole system within two months. Start small. Most households need only a handful of categories to cover the bulk of their lumpy expenses.

High-priority categories

- Annual or semi-annual insurance premiums (auto, home, renters, umbrella). These are large, predictable, and brutal if paid from a single paycheck.

- Car maintenance and repairs. Tires, brakes, registration, the occasional larger repair. Even newer cars cost something every year.

- Holidays and gifts. Combine birthdays, anniversaries, and end-of-year gifting into one fund and contribute year-round.

- Travel. Whether it's one big trip or several weekend ones, knowing the budget in advance changes how you plan.

Useful additions once the basics are funded

- Home maintenance. Appliances, HVAC servicing, small repairs. A rough rule many homeowners use is 1% of the home's value per year, though actual costs vary widely.

- Medical and dental. Deductibles, copays, glasses, anything not covered by insurance.

- Pet care. Annual vet visits plus a buffer for the unexpected.

- Subscriptions and annual memberships. Software renewals, warehouse club fees, professional dues.

- Replacement fund. Phones, laptops, mattresses — anything you know will need replacing every few years.

How to size each fund

The formula is simple: estimate the annual cost, divide by 12, and that's your monthly contribution. If the expense is due in fewer than 12 months, divide by however many months are left.

For example, if your auto insurance renewal is $900 and is due in nine months, you'd set aside $100 a month. If holiday spending typically runs $600, you'd save $50 a month all year.

Two practical tips:

- Look at last year's actual spending rather than guessing. Pull bank and card statements for the previous 12 months and total each category. Most people underestimate.

- Add a 10–15% buffer on top of your estimate. Prices drift, and a slightly over-funded category is a much better problem than a shortfall.

Where to keep the money

Sinking fund money should be liquid, safe, and ideally earning at least a little interest. A high-yield savings account at an online bank is the most common choice. Some banks let you create multiple labeled sub-accounts inside a single login, which makes tracking each category much easier than juggling one mixed pot.

If your bank doesn't offer sub-accounts, a single savings account paired with a simple spreadsheet works equally well. The spreadsheet tracks what each dollar is mentally assigned to, even though it all lives in one place. Budgeting apps that support "envelopes" or "buckets" can automate this if you prefer.

What we'd avoid: keeping sinking fund money in checking (it gets spent), in a brokerage account (market swings can hurt short-term goals), or in cash at home (no interest, and easy to raid).

Automating the system

Sinking funds work best when contributions are automatic. Once you've calculated your monthly totals, set up a recurring transfer from checking to savings on the day after payday. The money moves before you can spend it, and the system runs itself.

A quick monthly check-in — fifteen minutes is plenty — handles the rest:

- Confirm the transfer went through.

- Log any sinking fund expenses (e.g., "$340 from car repair fund for new brakes").

- Adjust contributions if any category is consistently over- or under-funded.

Common mistakes we see

- Too many categories at once. Starting with twelve funds is a recipe for quitting. Begin with three or four and add as you go.

- Raiding the funds for other spending. The whole system collapses if "car repair" money pays for dinner out. If a category is consistently overfunded, lower the contribution officially instead of borrowing informally.

- Forgetting to refill after a big withdrawal. After paying that insurance bill, the fund is at zero and needs to start rebuilding for next year immediately.

- Treating sinking funds as savings goals. They're not progress bars — they're earmarked spending. The money is meant to leave the account.

A realistic example

Imagine a household with these annual lumpy expenses: $1,440 auto insurance, $600 holidays, $900 car maintenance, $1,200 travel, $480 annual subscriptions. That's $4,620 a year, or $385 a month set aside into sinking funds.

If that number feels impossible, it's not because sinking funds don't work — it's because those expenses already exist, and they're currently being absorbed by credit cards, the emergency fund, or anxiety. Sinking funds just make the cost visible so you can decide what to keep, what to cut, and what to plan for honestly.

Editorial disclosure

This article is general personal-finance education, not financial advice. Individual situations vary, and tax, insurance, and savings strategies should be reviewed with a qualified financial professional who knows your full picture.

Key takeaways

- Sinking funds turn irregular expenses into predictable monthly contributions.

- Keep them separate from your emergency fund — emergencies are unknown, sinking funds are known.

- Start with three or four high-impact categories like insurance, car, holidays, and travel.

- Park the money in a high-yield savings account, ideally with labeled sub-accounts.

- Automate contributions on payday and review the system briefly each month.

- The goal isn't to grow the fund — it's to spend it as planned, calmly.

Frequently asked questions

What is a sinking fund in simple terms?

A sinking fund is money you set aside a little at a time for a specific expense you know is coming, like car insurance, holiday gifts, or a vacation. Instead of being surprised by the bill, you pay it from money you've already saved.

How is a sinking fund different from an emergency fund?

An emergency fund covers unexpected events like a job loss or sudden medical bill. A sinking fund covers expected expenses with a known date or rough timeline. Keeping them separate prevents you from draining your safety net for predictable costs.

How many sinking funds should I have?

Most people do well with three to seven active categories. Too few and you'll miss real expenses; too many and the system gets exhausting. Start with your biggest annual bills and add categories only as you spot recurring pain points.

Where should I keep sinking fund money?

A high-yield savings account is a common choice because the money earns interest and stays liquid. Some banks let you create labeled sub-accounts, which makes tracking each category easier without juggling multiple institutions.

Do I need a budgeting app to use sinking funds?

No. A simple spreadsheet works fine if you list each category, target amount, deadline, and monthly contribution. Apps can automate the math, but the discipline matters more than the tool.

What if I can't fund every category at once?

Prioritize the categories with the closest deadlines or largest amounts first, like annual insurance or holidays. Once those are funded, redirect contributions to the next priority. Sinking funds are a habit, not a sprint.