High-Yield Savings in 2026: Make Cash Work Harder

High-yield savings accounts can quietly add hundreds to your bottom line each year. Here's how to choose, structure, and use them well in 2026.

TL;DR: A high-yield savings account (HYSA) is one of the simplest, safest ways to make idle cash work harder in 2026. By moving your emergency fund and short-term savings into a federally insured account that pays a competitive APY, you can earn meaningfully more interest than a traditional savings account — often the difference between a few dollars a year and a few hundred. The trick is choosing the right account, structuring your money into clear buckets, and reviewing your rate every few months.

Most of us were taught to save, but very few of us were taught where to save. That gap is where a lot of money quietly leaks out of household budgets. Our team has been tracking the savings landscape closely heading into 2026, and the headline is simple: if your cash is sitting in a traditional checking or legacy savings account, you're almost certainly leaving money on the table.

Why high-yield savings matter more in 2026

Interest rates have been a moving target for several years. While no one can predict exactly where rates will sit by the end of 2026, the gap between what big traditional banks pay on standard savings and what online banks and credit unions pay on high-yield accounts remains substantial. That gap is what makes a HYSA worth setting up — not the absolute number on the rate sheet.

Consider the practical difference. A traditional savings account paying a fraction of a percent on a $10,000 balance might earn you the cost of a coffee over a year. The same balance in a competitive high-yield account can earn the equivalent of a nice dinner out every single month. The money is identical. Only the address it lives at has changed.

What exactly is a high-yield savings account?

A high-yield savings account is a deposit account that pays a notably higher annual percentage yield (APY) than the national average. They're most commonly offered by:

- Online-only banks, which have lower overhead than branch networks and pass some of those savings to depositors.

- Credit unions, which are member-owned and often offer competitive rates on share savings accounts.

- Fintech platforms that partner with FDIC-insured banks to hold customer funds.

Functionally, a HYSA behaves like any other savings account. You can deposit and withdraw, transfer to and from a linked checking account, and view your balance in an app. The key features to confirm are deposit insurance (FDIC for banks, NCUA for credit unions), no minimum balance traps, and no monthly maintenance fees.

HYSA vs. money market vs. CDs

These three cousins often get confused, so a quick clarifier:

- HYSA: Fully liquid, variable rate, easy transfers. Best for emergency funds and short-term goals.

- Money market account: Similar to a HYSA, sometimes with check-writing privileges. Rates are comparable.

- Certificate of deposit (CD): A fixed term and usually a fixed rate. You lock the money up for months or years in exchange for a guaranteed return. Best for cash you won't need before the term ends.

How to choose a high-yield savings account

The right account isn't always the one with the flashiest headline rate. We weigh these factors, in roughly this order:

- Insurance status. Confirm FDIC or NCUA coverage in writing. For fintech apps, find the partner bank named in the disclosures.

- APY consistency. Some banks lure new customers with a teaser rate that drops after a few months. Look for institutions with a track record of staying competitive.

- Fees and minimums. The best accounts charge no monthly fee and require no minimum balance. Read the fine print on excess withdrawal fees.

- Transfer speed. If you'll use this as an emergency fund, you want ACH transfers that arrive within one to two business days.

- App and customer service. A clean app and reachable humans matter when something goes wrong.

- Sub-account or "bucket" features. Some banks let you split one account into labeled goals, which is genuinely useful for budgeting.

Red flags to watch

- Rates that require you to maintain a checking account, direct deposit, or debit card spending threshold to qualify.

- Tiered rates where only the first few thousand dollars earn the advertised APY.

- Promotional bonuses with vague terms or long lock-in requirements.

- Unclear answers about who actually holds your money.

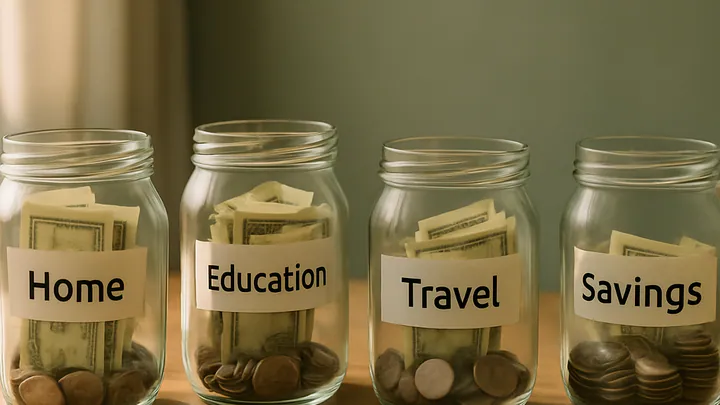

How to structure your cash in 2026

Once you've opened a HYSA, the next question is what to put in it. We like a simple three-bucket framework that keeps each dollar pointed at a clear job.

Bucket 1: Everyday checking

Keep roughly one month of essential expenses in your primary checking account. This handles bills, rent, groceries, and the unpredictable rhythm of daily spending. It doesn't need to earn a competitive yield — it needs to be frictionless.

Bucket 2: Emergency fund (HYSA)

This is the core use case. Aim for three to six months of essential expenses, held in a high-yield savings account at a different institution from your checking. The slight friction of needing to transfer the money out is a feature, not a bug: it discourages impulse withdrawals while still being available within a day or two if you genuinely need it.

Bucket 3: Short-term goals (HYSA or CDs)

Money you'll spend within the next one to three years — a wedding, a down payment, a car replacement, a major trip — doesn't belong in the stock market. The risk of a bad year right before you need the cash is too high. A HYSA with labeled sub-accounts, or a small CD ladder, is the right home. This is also where sinking funds live: small monthly contributions toward predictable annual expenses like insurance premiums or holiday gifts.

Common mistakes to avoid

- Chasing rates obsessively. Moving accounts every time someone offers ten extra basis points wastes hours and rarely changes your life. Pick a reputable account and review it twice a year.

- Holding too much cash. A HYSA is excellent for safety and liquidity, but cash generally doesn't outpace inflation over the long run. Money you won't need for five or more years usually belongs in a diversified investment account, not in savings.

- Forgetting about taxes. Interest earned is typically taxable as ordinary income. The headline APY is a gross number — your after-tax return will be lower.

- Mixing goals in one account. When the emergency fund and the vacation fund share an account, the vacation usually wins. Labeled buckets or separate accounts protect each goal from the others.

- Never automating. A small recurring transfer from checking to savings on payday is the single most reliable savings habit we've seen. Manual saving works for a few months, then real life intervenes.

A simple 30-minute setup

If you've been meaning to do this, here's a realistic plan you can finish in one sitting:

- Spend ten minutes comparing two or three high-yield savings accounts. Confirm insurance, fees, and APY.

- Open the account online. Most applications take five to ten minutes and a government ID.

- Link your existing checking account and make a small starter transfer.

- Set up an automatic recurring transfer for the day after each payday — even $50 to start.

- Add a calendar reminder for six months from now to review the APY and your savings target.

That's it. The hard part is starting, not optimizing.

Key takeaways

- A high-yield savings account is the simplest upgrade most people can make to their cash strategy in 2026.

- Prioritize federal insurance, low fees, consistent rates, and fast transfers over the flashiest headline APY.

- Use separate buckets for everyday spending, emergencies, and short-term goals so each dollar has a job.

- Automate contributions, then review your rate and balance every six months rather than every week.

- Cash you won't need for many years generally belongs in long-term investments, not savings.

Editorial disclosure: This article is for general educational purposes only and does not constitute financial, tax, or investment advice. Interest rates, fees, and account terms vary by institution and change frequently. Before opening or moving accounts, review current disclosures from the bank or credit union and, if your situation is complex, consult a qualified financial advisor or tax professional.

Frequently asked questions

What is a high-yield savings account?

A high-yield savings account is a deposit account, usually offered by an online bank or credit union, that pays a much higher annual percentage yield than a traditional brick-and-mortar savings account. Your money remains liquid and federally insured up to applicable limits.

Are high-yield savings accounts safe?

Yes, as long as the account is held at an FDIC-insured bank or NCUA-insured credit union and your balance stays within insured limits, typically $250,000 per depositor, per institution. The bank invests conservatively to support the rate it pays you.

How often do high-yield savings rates change?

Rates can change at any time without notice and tend to move in step with broader interest rate trends. It's worth checking your APY every few months to make sure your bank is still competitive.

Should I keep my emergency fund in a high-yield savings account?

For most people, yes. A high-yield savings account keeps the money liquid, accessible within a day or two, and protected from market swings, which is exactly what an emergency fund needs to do.

Is interest from a high-yield savings account taxable?

In most jurisdictions, yes. Interest is typically treated as ordinary income and reported on your annual tax return. Your bank will usually send you a year-end tax form if you earned above a small threshold.

Can I have more than one high-yield savings account?

Absolutely. Many people use multiple accounts to separate goals, such as an emergency fund, a travel fund, and a home repair fund, which can make budgeting easier and reduce the temptation to dip into the wrong bucket.