Sinking Funds in 2026: Save Without the Stress

Sinking funds turn irregular expenses into predictable monthly habits. Here is how we build, automate, and protect them in 2026 so surprise bills stop derailing budgets.

TL;DR: Sinking funds are small monthly savings buckets earmarked for specific upcoming expenses — think car registration, holiday gifts, or a new laptop. By dividing each known cost by the months until it is due and automating the transfer, we turn financial surprises into predictable line items. In 2026, with high-yield savings accounts still paying competitive rates and most banks offering free subaccounts, sinking funds are one of the highest-leverage budgeting habits we can build this year.

Most budgets do not fail because we overspend on groceries. They fail because a $740 car repair, a $300 vet visit, or a $1,200 holiday season arrives and there is nowhere to pull the money from except a credit card. Sinking funds fix that pattern. Below, our team walks through exactly how to set them up, what categories matter most, and how to keep the system running when life gets noisy.

What a sinking fund actually is

A sinking fund is a pool of money you contribute to gradually so that a known, future expense is fully paid for by the time it arrives. The term comes from corporate finance, where companies set aside cash to retire a bond or replace equipment. For households, the mechanics are the same: identify a future cost, divide it across the months you have, and save that amount automatically.

The key word is known. A sinking fund is not for surprises — that is what an emergency fund is for. A sinking fund is for the expenses we can see coming on a calendar but routinely pretend we cannot.

Sinking fund vs. emergency fund

- Emergency fund: Covers truly unexpected events — job loss, urgent medical care, a roof leak. Most planners, including those at Fidelity and Vanguard, suggest three to six months of essential expenses.

- Sinking fund: Covers planned, irregular costs. You know they are coming; you just do not want them to land in a single painful month.

Both belong in your financial system. The emergency fund is your shock absorber. Sinking funds are your shock preventers.

Why sinking funds matter more in 2026

Two shifts make this year a strong moment to commit to the habit. First, the U.S. Bureau of Labor Statistics has reported persistent year-over-year increases in service categories like auto insurance and home maintenance, meaning the bills that traditionally hurt households are still climbing faster than headline inflation. Second, a 2024 Bankrate survey found that a majority of U.S. adults would not cover a $1,000 emergency from savings — a vulnerability that sinking funds directly reduce by pre-funding the expenses people typically charge to credit cards.

There is also a behavioral angle. Research summarized by the Consumer Financial Protection Bureau consistently shows that people who use labeled, goal-specific savings accounts save more than those using a single general account. Naming the money changes how we treat it.

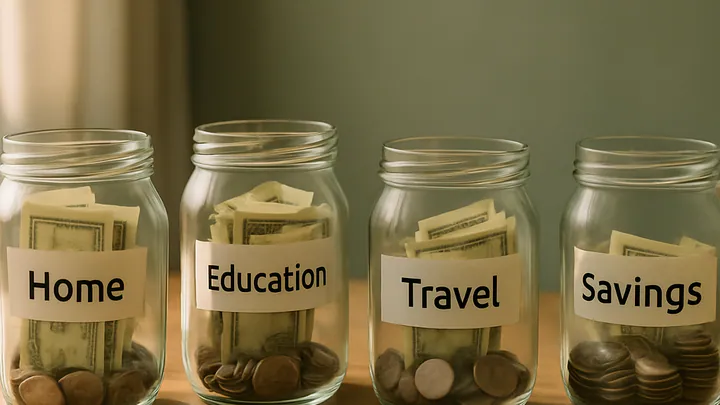

The categories worth funding first

You do not need fifteen sinking funds. Most households get 80% of the benefit from a focused handful. We recommend starting with these:

- Auto: Insurance premiums, registration, tires, and routine repairs. Even a reliable car costs money to keep on the road.

- Home or rental: Appliance replacement, HVAC service, renter's insurance, small repairs. Homeowners typically spend 1–3% of the home's value annually on upkeep.

- Holidays and gifts: December alone can wipe out months of progress without a plan. Birthdays, anniversaries, and teacher gifts add up too.

- Medical and dental: Deductibles, prescriptions, glasses, copays. Even with good insurance, out-of-pocket costs are predictable in aggregate.

- Annual subscriptions and memberships: Software renewals, gym fees, Costco, professional dues. These often hit on the same month every year.

- Travel: Even one trip a year benefits from a dedicated fund so you are not financing memories at 24% APR.

If you have pets, kids in activities, or a wedding on the horizon, add one fund per major category. Stop there for the first six months.

How to calculate each contribution

The math is intentionally boring. For every category, list the expected annual total and divide by twelve. If something is due in fewer months, divide by the months remaining instead.

Example: Your six-month auto insurance premium of $720 is due in August. It is currently February. You have six months, so transfer $120 per month into the auto sinking fund. When August arrives, the bill pays itself.

To estimate categories you have never tracked, review the last twelve months of bank and card statements. The numbers are almost always higher than people guess — and that is exactly why this exercise is worth doing.

Where to keep the money

Sinking funds belong in a savings account that is separate from your checking but still easy to reach within a day or two. As of 2025–2026, several online banks and credit unions offer high-yield savings accounts with the ability to create labeled subaccounts or "buckets" inside a single account. Ally Bank's buckets and Capital One's 360 Performance Savings subaccounts are commonly cited examples, but many regional credit unions now offer similar features.

The two non-negotiables: the account should be FDIC- or NCUA-insured, and it should earn meaningfully more than a standard checking account. Earning a competitive yield on a $5,000 combined sinking fund balance can quietly add a hundred-plus dollars a year — money that essentially pays you to be organized.

Automate before motivation fades

Set a recurring transfer for the day after each payday. If you wait to move money manually, the system will fail within two months. Automation is the entire point: you are paying future-you on a schedule so present-you does not have to make a decision.

Common mistakes we see

- Starting with too many funds. Three to five categories is enough to feel meaningful progress. You can add more in month four.

- Underfunding the first cycle. If insurance is due in three months, you need to catch up faster than 1/12 per month. Be honest about timing.

- Borrowing from one fund to feed another. Occasionally necessary, but if it becomes a pattern, the amounts are wrong. Recalculate rather than rob.

- Forgetting to refill after spending. When a sinking fund pays a bill, the cycle restarts immediately for next year. Keep the automation running.

- Mixing sinking funds with the emergency fund. Keep them visually and mentally distinct so neither gets raided for the wrong reason.

A simple 30-day setup plan

- Week 1: Pull last year's statements and list every irregular expense over $100. Total each category.

- Week 2: Open a high-yield savings account with subaccounts (or open separate accounts if your bank does not support buckets).

- Week 3: Calculate monthly contributions and schedule automatic transfers for the day after payday.

- Week 4: Add the funds to your budget as fixed line items — they are now bills you pay to yourself.

By the end of the month, the system is doing the work. Your job for the rest of the year is to leave it alone and let the automation compound.

Key takeaways

- Sinking funds turn known irregular expenses into predictable monthly habits.

- Start with three to five categories — auto, home, holidays, medical, and travel are common winners.

- Divide each annual cost by the months until it is due, then automate the transfer.

- Keep the money in an insured high-yield savings account, ideally with labeled buckets.

- Refill the fund after each use so next year's bill is already handled.

- Sinking funds complement — they do not replace — an emergency fund.

Editorial disclosure: This article is for general educational purposes and is not financial advice. Individual circumstances vary, and the right savings strategy depends on your income, debts, and goals. For personalized guidance, please consult a qualified financial advisor or a nonprofit credit counselor accredited by the NFCC.

Frequently asked questions

What is a sinking fund in personal finance?

A sinking fund is money you set aside in small monthly amounts to pay for a specific expected expense, like car insurance, holiday gifts, or a vacation. It spreads a large irregular bill over the year so it never hits your budget all at once.

How is a sinking fund different from an emergency fund?

An emergency fund covers unexpected events like job loss or a medical bill, and is usually 3–6 months of expenses. A sinking fund covers known, planned costs you can predict in advance, such as annual subscriptions or a wedding.

Where should I keep my sinking funds?

Most savers use a high-yield savings account with subaccounts or labeled buckets so each goal is visible. Keeping the money separate from checking helps reduce the temptation to spend it on something else.

How many sinking funds should I have?

Start with three to five categories tied to your biggest irregular expenses, then expand as you get comfortable. Too many funds at once can feel overwhelming and lead to abandonment within a few months.

How much should I put into each sinking fund per month?

Divide the total expected cost by the number of months until you need the money. For a $600 car insurance premium due in 12 months, you would save $50 per month into that fund.

Are sinking funds worth it if I have debt?

Yes, modest sinking funds can prevent new debt from forming when irregular bills arrive. Many financial educators suggest building small sinking funds alongside debt payoff so a surprise expense does not push you backward.