Sinking Funds in 2026: Budget Without the Stress

Sinking funds turn unpredictable expenses into calm, planned line items. Here is how to set them up in 2026 without overcomplicating your budget.

TL;DR: Sinking funds are small, purpose-labeled savings buckets you contribute to gradually so predictable-but-irregular expenses — car repairs, holidays, annual insurance, a new phone — never blow up your monthly budget. In 2026, the easiest setup is a high-yield savings account with named sub-accounts, three to eight active categories, and an automatic transfer that runs the day after payday. Done right, sinking funds turn financial surprises into scheduled line items and quietly remove most of the stress from budgeting.

Most people do not have a spending problem. They have a timing problem. Rent, groceries, and streaming subscriptions arrive on a rhythm we plan for. Then February brings the car registration, June brings the wedding invitation, and November brings the boiler that finally gives up. The money was technically there — just not in the right place at the right moment.

Sinking funds fix the timing. Our team has watched readers use this one simple structure to stop living paycheck-to-paycheck without earning more, cutting joy, or downloading a new app every quarter. Here is how to make them work in 2026.

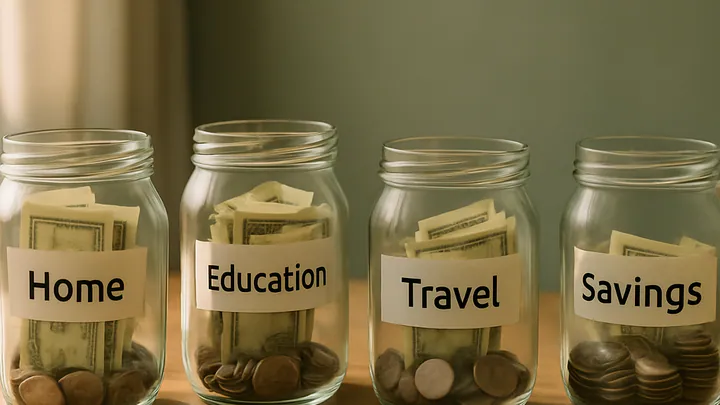

What a sinking fund actually is

A sinking fund is a labeled pot of money you build up slowly for a specific future expense. The term comes from corporate finance, where companies set aside cash over time to retire a bond or replace equipment. The personal-finance version works the same way: you know a cost is coming, you know roughly when, and you fund it in small predictable pieces instead of one painful lump.

The distinction that matters most is this:

- Emergency fund — for the unknown. Job loss, urgent medical bills, a broken furnace in a rental you did not expect to need to fix.

- Sinking fund — for the known but irregular. Car insurance renewal, Christmas gifts, a family trip in August, your annual professional license.

Mixing the two is where budgets quietly fall apart. If holiday shopping drains your emergency fund every December, you are not protected against actual emergencies in January.

Why 2026 is a good year to set them up

Two shifts make sinking funds more useful now than they were even a few years ago. First, high-yield savings accounts remain broadly available, so parked cash actually earns something meaningful while it waits. Second, more banks and neobanks let you create named sub-accounts or "buckets" inside a single savings account, which removes the biggest historical friction — tracking which dollars belong to which goal.

You no longer need a spreadsheet with color-coded columns to run this system. You need one account and a recurring transfer.

Choose your categories carefully

The temptation is to create a sinking fund for everything. Resist it. Too many buckets makes the system feel like admin, and admin is what people quit first. Start by listing every non-monthly expense from the past twelve months. Look at bank statements, not memory — memory undercounts.

Common high-value categories worth funding:

- Vehicle — insurance renewal, registration, tires, routine maintenance, one "something broke" cushion.

- Home — property taxes, appliance replacement, seasonal maintenance, a small repairs float if you rent.

- Gifts and holidays — birthdays, Christmas or Diwali or Eid, weddings, teacher gifts.

- Travel — a planned trip with a known month, plus a smaller "unexpected travel" fund for weddings and funerals.

- Annual subscriptions and memberships — software, warehouse clubs, professional dues, domain renewals.

- Health and wellness — dental work, glasses, deductibles, therapy copays.

- Technology replacement — the phone, laptop, or camera you know will need replacing within two years.

The three-to-eight rule

Pick the three to eight categories that most reliably derail your budget. If gifts and car costs are consistently the culprits, start there. You can always add more later; you rarely successfully manage more than eight at once.

Calculate the monthly contribution

For each category, estimate the annual total and divide by twelve. That is your baseline monthly contribution.

Example:

- Car insurance renewal: roughly £900 per year → £75 per month

- Holiday gifts: roughly £600 → £50 per month

- Annual trip: roughly £1,800 → £150 per month

- Tech replacement: roughly £1,200 every two years → £50 per month

Add a modest buffer — five to ten percent — because your estimate is almost certainly optimistic. If the total is uncomfortably high, that is useful information: your lifestyle costs more than a naive month-to-month view suggests. Better to see it now than in a crisis.

What if you are starting mid-year?

Divide the remaining cost by the months until you actually need it. If your insurance renews in five months and you need £900, that is £180 per month, not £75. Front-load aggressively on the closest deadlines, then settle into a steady monthly rate once each fund catches up.

Set it up in one sitting

Sinking funds fail when they live in your head. They succeed when they live in an account.

- Open a high-yield savings account that supports named sub-accounts or goals if your current bank does not. Many online banks offer this at no cost.

- Create one bucket per category and label it clearly — "Car 2026," "Gifts," "Summer Trip." Vague labels invite raiding.

- Automate one transfer per payday that funds all buckets at once. If your bank does not split automatically, transfer the total and reallocate in the app.

- Pay from the fund, not around it. When the expense arrives, move the money back to checking and pay the bill. Do not leave the expense on a credit card "just for the points" if you will forget to reimburse yourself.

Common mistakes to avoid

We see the same pitfalls repeatedly, and they are almost all fixable in an afternoon.

- Underestimating annual totals. Look at last year's actual spend, not what you wish it had been.

- Raiding the fund for the wrong purpose. The gifts fund is not the "I had a rough week" fund. Naming buckets specifically helps.

- Skipping the buffer. Tires cost more than you think. So does everything else.

- Running too many buckets. If you dread opening the app, you have too many. Consolidate.

- Keeping the money in checking. It will get spent. Separation is the entire point.

Sinking funds for irregular income

If you are self-employed, freelance, or work on commission, sinking funds are even more valuable — but the mechanics shift. Instead of a fixed monthly amount, assign each category a percentage of every deposit. For example: 8% of every client payment to taxes, 4% to car, 3% to gifts, 5% to tech replacement. Route the transfers the same day money hits your account, before it feels like available cash.

When to stop, pause, or reallocate

Sinking funds are not sacred. Once a bucket exceeds the annual target by more than roughly twenty percent, pause contributions and redirect the money elsewhere — high-interest debt, your emergency fund, or investing. Reassess every category once a year, ideally in January, and again after any major life change: new job, new home, new baby, new city.

Key takeaways

- Sinking funds solve timing, not income. They convert irregular expenses into calm monthly line items.

- Keep them separate from your emergency fund — the two do different jobs.

- Three to eight named buckets in a high-yield savings account is the sweet spot for most households.

- Automate one transfer per payday and pay expenses from the fund, not around it.

- Review categories annually and reallocate any bucket that consistently overshoots its target.

Editorial disclosure: This article is general personal-finance education, not financial advice. Your situation — including tax rules, debt obligations, and account availability in your country — may change the right approach. For decisions involving significant sums, taxes, or debt strategy, please consult a qualified financial advisor or accountant licensed in your jurisdiction.

Frequently asked questions

What is a sinking fund in simple terms?

A sinking fund is money you set aside gradually for a specific future expense you know is coming, like car insurance, holidays, or a new laptop. Instead of getting hit with a big bill, you contribute small amounts over time so the money is already there.

How is a sinking fund different from an emergency fund?

An emergency fund covers unexpected events like job loss or a medical emergency. A sinking fund covers expected but irregular expenses with a known purpose and rough date, such as annual property taxes or a planned vacation.

How many sinking funds should I have?

Most people do well with three to eight active sinking funds. Fewer than three often misses key irregular expenses, while more than eight can become tedious to maintain. Focus on the categories that consistently derail your budget.

Where should I keep sinking fund money?

A high-yield savings account is usually the best fit because the money earns interest, stays liquid, and is separated from your checking account. Some banks let you create named sub-accounts, which makes tracking each fund much easier.

Do sinking funds work if my income is irregular?

Yes, but the approach shifts. Instead of contributing a fixed monthly amount, you fund each category as a percentage of income received. On higher-earning months you catch up or get ahead, and on leaner months you contribute less.

Should I invest sinking fund money instead?

Generally no. Sinking funds are for short-term, near-certain expenses within roughly two years. Market volatility can leave you short right when you need the money. Keep these funds in cash or cash-equivalent accounts.